The best moment to start your next growth engine is when your current one is still climbing — which is precisely when every instinct and every spreadsheet tells you not to.

A company at the top of its game is in more danger than a company in obvious trouble. The one in trouble knows it has to change. The one at its peak has every reason not to — the numbers are good, the team is confident, the strategy is "working." That confidence is the problem. It's the most expensive moment to be complacent and the one where complacency feels most justified.

Every growth engine follows an S-curve: a slow start, a steep climb, a plateau, a decline. This is true of products, channels, business models, entire companies. The uncomfortable strategic fact is that the time to build the next curve is partway up the current one — while it's still climbing, still funding you, still making you look smart. Wait until the first curve rolls over and you're trying to build the future with declining resources, a spooked team, and no time. The gap between those two moments is where most good companies quietly lose the next decade.

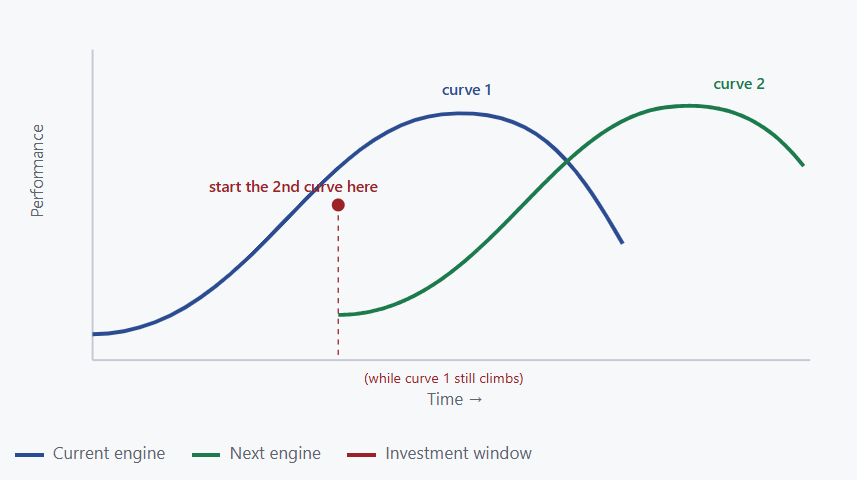

Visual 1 — The handoff happens before the peak

The model: the second curve has to be started during the first curve's ascent, because it begins below the first and takes time to climb. Begin at the peak and the handoff lands in a trough. Begin during the decline and there may be no handoff at all.

The timing is hard because the incentives fight it

Knowing this and acting on it are different things, because the second curve always arrives looking worse than the first. It's small, unproven, lower-margin, and it competes for resources with a core business that is — by every current metric — the better use of money. Any honest spreadsheet will tell you to keep feeding the winner. The board, the team, and your own judgment all point at the first curve, because right now it is the better bet. The second curve only wins on a timeline most decision-making refuses to use.

So the investment gets deferred, reasonably, quarter after quarter — until the core plateaus and suddenly everyone wants the next engine that should have been started two years ago. This is why incumbents rarely die of stupidity. They die of sensible, well-defended decisions to keep backing the thing that was working, made right up until it stopped.

Why the curves are getting shorter

This was always the pattern. Two forces have sharpened it.

The first is the pace of disruption — AI in particular is compressing how long any given advantage lasts. Curves that used to plateau over a decade now do it in years. A shorter first curve means a shorter window to start the second, and less margin for getting the timing wrong.

The second is the cost of capital. In the cheap-money years, a company that missed the second-curve window could often buy its way back in — acquire the disruptor, fund a crash program, raise to cover the gap. With capital now priced at a structurally higher level, that escape hatch is more expensive and less available. The penalty for late is steeper than it was, which makes building early — out of your own cash flow, while you still have it — the cheaper path by far.

The honest cost: it will look like a mistake for a while

The contrarian truth most "innovate early" advice skips is that doing this right will feel wrong for a real stretch. The second curve will underperform the first on every metric that matters today. You'll divert your best people from the proven business to an unproven one. You may cannibalize your own revenue before a competitor does it for you. For several quarters, the disciplined move and the foolish move are indistinguishable from the outside — and from most internal dashboards.

The dip is not a sign you got it wrong. The dip is the price of admission to the next curve. Companies that refuse to pay it aren't being prudent — they're financing a more expensive collapse later.

That's the actual strategic courage here: not the vision to see the next curve, which plenty of leaders have, but the willingness to fund it through the period where it makes you look worse, not better.

What this means for leaders

Judge the timing off the current curve's slope, not its height. The trigger to invest isn't "the core is declining" — by then you're late. It's "the core's growth rate is starting to flatten even though the absolute numbers are still great." That early bend is the signal. Watch the second derivative, not the headline.

Fund the second curve from a separate budget and protect it from the first curve's metrics. If the new engine has to justify itself quarterly against the mature business's margins, it will lose every time and die in committee. Ring-fence the resources and judge it on its own curve, on a longer clock.

And put real people on it, not spare capacity. The surest way to guarantee the second curve fails is to staff it with whoever isn't busy and let the core keep all the talent. The next business deserves some of your best people while the current one can still spare them — because the moment it can't, it's already too late to ask.

Builds on Charles Handy's "second curve" concept, applied to the 2026 environment of compressed advantage cycles and a higher cost of capital. Macro context: Norton Rose Fulbright, Cost of Capital: 2026 Outlook.