Every strategy deck claims a moat. Most of what gets called one is a temporary lead that competitors can copy by next year. Mistaking the two is how companies get blindsided.

Sit through enough board meetings and you'll hear the word so often it stops meaning anything. The product has a moat. The brand is a moat. The data is a moat. The team, somehow, is a moat. By the end of the quarter, everything the company owns has been promoted to a structural defense, and the word that once described a specific kind of durability now describes a feeling.

That feeling is the problem. "Moat" has become the term leaders reach for when they want to stop worrying about competition. It's a tranquilizer disguised as analysis.

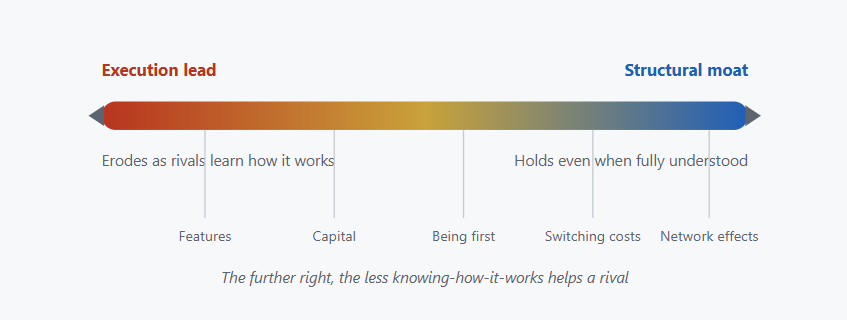

Warren Buffett gave us the metaphor to describe something narrow and rare: a structural reason a competitor can't take your castle even when they can see exactly how it's defended. Most of what gets labeled a moat fails that test on contact. It's a lead, not a defense — and a lead, by definition, is something the field can close.

The test that settles it

There's a single question that separates a moat from a head start, and it's unforgiving: Could a well-funded, competent rival replicate this advantage even if they knew exactly how it worked?

If the answer is yes — given enough money, talent, and a year or two — what you have is an execution lead. That can be valuable. Leads buy time, and time can be spent building something more durable. But a lead is not a moat, and treating it like one is where the trouble starts. You stop running because you think the water protects you, and you don't notice the rival has already drained it.

The reason the distinction matters is that the two demand opposite behavior. A lead says: move faster, the clock is running. A moat says: the structure holds, invest in widening it. Confuse them and you'll relax precisely when you should sprint.

Visual 1 — The audit

What gets called a moat | What it usually is | The real test it fails (or passes) |

|---|---|---|

"Our features are ahead" | An execution lead | A funded rival can ship the same feature set in a year. Fails. |

"We raised more capital" | A spending advantage | Money is the most copyable input there is. Fails. |

"We got here first" | A timing position | Being early protects nothing once the path is cleared. Fails. |

"Everyone knows our logo" | Awareness, not preference | Recognition a competitor can buy is not a moat. Mostly fails. |

"Switching costs us our customers real money" | Structural lock-in | A rival who knows this still can't make switching cheap. Passes. |

How to read it: run every claimed advantage through the last column. The honest ones that survive are short. Most claimed moats are execution leads wearing a borrowed word.

What isn't a moat, no matter how it feels

Features aren't. A feature is a recipe, and recipes leak. The competitor doesn't even have to reverse-engineer it; you'll demo it to them on a sales call. Whatever lead a feature buys is measured in release cycles, and release cycles are getting shorter, not longer.

Capital isn't. A funding lead feels like armor because the number is large. But money is the single most fungible thing in business — your rival can raise it too, and in a market where capital chases the same theme, often will. "We're better funded" describes this quarter's bank balance, not a defensible position.

Being first isn't. First-mover status is a timing fact, not a structural one. It protects you only if being early triggers something self-reinforcing — a network, a standard, a supply lock. Absent that mechanism, the pioneer mostly pays to educate a market the follower will harvest.

And brand-as-logo isn't. A recognizable name is awareness, not preference. The moat is in the preference — the reason a customer chooses you when the alternative is cheaper and adequate. If your "brand moat" is really just ad spend that a competitor with a checkbook can match, it was never a moat. It was a media budget.

What actually holds

Real moats are boring, structural, and few. Network effects, where the product gets more valuable as more people use it, so a rival has to overcome not your features but your users. Switching costs, where leaving you is genuinely expensive — in data, retraining, integration, risk — regardless of how good the alternative looks. Proprietary data that compounds, where your position generates information a competitor structurally can't get because they don't have your position. Scale economies, where being bigger makes your unit costs lower in a way a smaller rival cannot match by trying harder. And regulatory or structural barriers — licenses, contracts, physical assets — that exist whether or not anyone admires your strategy.

Notice what they share. In each case, the competitor can know precisely how the advantage works and still be unable to copy it, because copying it requires something they don't have and can't simply buy: your users, your customers' sunk investment, your accumulated data, your installed scale. That's the line. Knowledge doesn't dissolve a real moat. It dissolves a lead.

Visual 2 — From lead to moat

Conceptual model. Durability isn't binary; it's a spectrum. The same advantage that protects you today may sit on the eroding end. Plot your "moats" honestly and most will land left of center.

The contrarian part

Here's what makes this dangerous rather than merely sloppy. Many of the most celebrated moats in business history were, at the moment they were celebrated, just execution leads. The companies that survived treated them as leads and kept building. The ones that didn't believed their own decks.

The thing that disrupts you is rarely a better product. It's the complacency you bought yourself by calling a head start a moat — and then stopped running.

This is why the inflation of the word is not harmless. A leader who believes the castle is protected stops reinforcing the walls. A leader who knows it's only a lead behaves like someone still in a race, because they are. The label changes the behavior, and the behavior decides the outcome long before the competitor arrives.

What this means for leaders

Audit the word, not just the strategy. Go through every place your team has written or said "moat" this year and apply the one test: could a funded rival copy this knowing how it works? Most of what survives the cut will be uncomfortable in its smallness. That discomfort is accurate.

Treat leads as leads — assets with an expiry date. A lead is real and worth having, as long as you spend it buying something durable before it erodes. The question for any advantage isn't "do we have it?" but "what structural thing are we converting it into while it lasts?"

And remember the rules changed with the cost of money. When capital was free, you could fund your way to the appearance of a moat — outspend rivals into submission. At a structurally higher cost of capital, that route is closed. You can't out-spend your way to safety anymore. What's left is the unglamorous work of building advantages a competitor can understand completely and still be unable to take.

The companies that compound through the next cycle won't be the ones with the most moats on the slide. They'll be the ones honest enough to admit how few they actually have, and disciplined enough to keep running on the rest.

A LookatBusiness original.