Every strategy deck is a list of things to add. The companies that actually compound are the ones with a longer list of things they've agreed not to.

Pull up almost any company's growth strategy and you'll find the same shape: a list of additions. New segment, new geography, new product line, new partnership, new channel. Strategy, as most teams practice it, is the art of saying yes to more things in an orderly sequence.

That's not strategy. That's a wish list with a Gantt chart.

The companies that compound fastest tend to do the opposite of what the deck implies. They grow by subtraction — by being unusually disciplined about the customers they turn away, the markets they decline, and the obviously-reasonable ideas they kill before launch. I call the return on that discipline the Focus Dividend: the compounding advantage you earn from what you deliberately refuse to do.

The math nobody puts on the slide

Focus isn't a personality trait. It's an allocation decision with a measurable payoff.

A company running four serious initiatives gives each a quarter of its attention, its best people, and its credibility with customers. Spread the same resources across nine, and every bet gets thinner — not just in budget, but in the scarce things that actually decide outcomes: senior attention, engineering depth, the patience to let a thing work. Most "growth" portfolios quietly starve their best bet to keep five mediocre ones on life support.

The subtraction math is unintuitive because addition feels safe. Adding an initiative looks like ambition and costs nothing today. Killing one looks like retreat and the cost is immediate and personal — someone's project, someone's headcount, someone's quarter. So the additions accumulate and the subtractions never happen, and a year later the company is busier, broader, and growing slower than the focused competitor it used to lead.

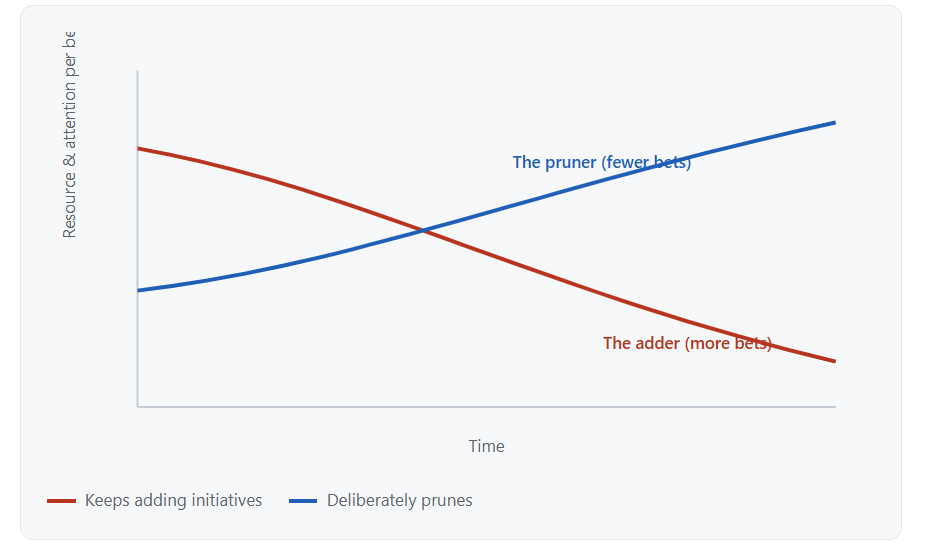

Visual 1 — The Focus Dividend

Conceptual model. Two companies, same resources. The one that keeps adding starves every bet; the one that prunes concentrates force. Same inputs, opposite trajectories — that gap is the dividend.

Why this is the year to get ruthless about it

The macro backdrop has quietly changed the cost of being unfocused.

When capital was cheap, breadth was nearly free — you could fund five experiments and let the market sort them out. That era is over. With the cost of capital sitting at a structurally higher plateau and boards rewarding capital efficiency over raw expansion, every initiative now competes against a real hurdle rate. The unfocused portfolio isn't just slower anymore. It's expensive in a way it wasn't three years ago.

AI has made the problem worse, not better. It has lowered the cost of starting things — a prototype, a new vertical's content, a second product surface — which means the temptation to spread out has never been stronger. The constraint was never the ability to start. It's the capacity to finish something well. Cheap starts and scarce follow-through is exactly the recipe for a portfolio of half-built bets.

The three refusals

The Focus Dividend is earned in three places. Each is a "no" that feels like leaving money on the table — and that's precisely why most companies can't say it.

The customer no. The wrong customer doesn't announce itself. It arrives as revenue — a logo willing to pay, but only if you bend the roadmap, staff a custom integration, and reorganize support around its edge cases. Say yes a few times and your product becomes a committee of other people's requirements. The disciplined company turns that revenue away, because it can see the second-order cost the P&L can't.

The market no. Adjacent markets are seductive because they're plausible. "We already do X; Y is right next door." But adjacency is not the same as advantage. Entering a market where you're merely competent — rather than clearly better — taxes your core to subsidize a fight you'll likely lose. The best operators decline more good markets than they enter.

The product no. Every roadmap accumulates features that are individually defensible and collectively fatal. Each one made sense to someone. Together they bloat the product, confuse the buyer, and bury the one thing you do that nobody else does. Killing a shipped feature is organizationally painful, which is exactly why so few companies do it and so many products slowly turn to mush.

Visual 2 — The three refusals

Refusal | What saying yes really costs | Signal it's time to say no |

|---|---|---|

The customer no | Roadmap captured by one account's edge cases | You're building features only one logo will ever use |

The market no | Core business taxed to fund a fight you won't clearly win | Your pitch is "we're also pretty good at this" |

The product no | The thing you're best at gets buried under the merely useful | New users can't tell what the product is for |

How to use it: run your current growth plan through all three columns. The refusals you can't bring yourself to make are usually where the dividend is hiding.

The refusal that actually matters

Here's the part the productivity-guru version of "focus" gets wrong. Focus is not about doing one thing. Plenty of focused companies run several lines at once. The discipline isn't in rejecting the obviously bad idea — anyone can do that. It's in rejecting the plausible one.

The bad idea protects itself. The dangerous one wears a good business case, a credible champion, and a reasonable-looking TAM. Strategy is mostly the courage to say no to things that would have probably worked.

That's an uncomfortable standard, because it means passing on real opportunities — not fake ones. The adjacent market that a competent team could have made profitable. The big customer you could have served if you'd contorted a little. These are genuine forgone gains. The Focus Dividend is the bet that what you protect by refusing them is worth more than what you'd have earned by chasing them. Usually it is, because the thing you protect is the only thing compounding.

What this means for leaders

Put a kill list next to your roadmap. Most leadership teams maintain a meticulous list of what they're starting and no list at all of what they're stopping. The second list is the strategy. If nothing got cut this quarter, you didn't make a strategic choice — you made an addition and called it one.

Make the no's expensive to overturn and the yes's easy to question, not the reverse. In most companies it's the opposite: starting something needs a slide, killing it needs a fight. Flip the burden of proof and focus stops being a heroic act and becomes the default.

And measure the dividend where it actually shows up — not in the number of bets running, but in how much force is behind the one that matters most. The right question at the end of a planning cycle isn't "what are we adding?" It's "what does our best bet have now that it didn't have before?" If the honest answer is "less, because we spread out," you've paid the tax instead of earning the dividend.

Growth gets talked about as a function of ambition. It's closer to a function of refusal. The market doesn't reward the company that wanted the most. It rewards the one that finished something while everyone else was busy starting.

Context drawn from: Norton Rose Fulbright, Cost of Capital: 2026 Outlook, RSM, "When Money Has a Price", and Morgan Stanley Counterpoint Global, "Cost of Capital and Capital Allocation."