Founders celebrate the raise like a win. It's a bill, not a trophy — capital you've promised to turn into far more capital, on someone else's clock.

The Series A closes on a Thursday. By Friday there's a post — the logo, the round size, the lead investor, the line about being "thrilled to partner." The comments fill with confetti emojis. Somewhere in the founder's chest there's a feeling that reads a lot like having arrived.

That feeling is the problem. The money just landed in the account, and already it has done its first quiet bit of damage: it has been mistaken for an accomplishment.

A raise is not something you achieved. It's something you took on. You have just signed up to convert a pile of someone else's money into a much larger pile, inside a window you don't fully control, against a bar that just went up. The press release frames it as a finish line. It's a starting gun with a debt attached.

The celebration problem

Startup culture has built an entire ceremony around the wrong moment. We throw the party at the raise and stay quiet at the milestones that actually matter — the first time the product retains, the quarter where revenue covers payroll, the customer who renews without being chased. Those events change the company. The raise just funds the attempt.

The reason the raise gets the party is that it's legible. It's a number, it has a date, and it comes with a counterparty who validated you with a check. Real progress is mushier and slower and harder to screenshot. So founders over-index on the thing that photographs well, and a generation of operators has internalized a quiet, corrosive belief: that getting funded is the same as being good.

It isn't. Plenty of companies that raised enormous rounds are gone. The check was never evidence the business worked. It was a bet that it might.

What a raise actually obligates you to

When you take institutional money, you are not borrowing patience. You are selling a claim on a future that you now have to manufacture. Venture capital is priced for outliers, which means your investors didn't fund the company you have. They funded the company you promised to become — and that promise has terms, even when nobody writes them on the term sheet.

The first term is growth. Not growth in the abstract, but the specific, compounding, venture-scale curve that justifies the price they paid. The second is time. A round buys you a runway, and the end of that runway is not "when the money runs out." It's the moment, roughly twelve months earlier, when you need to show enough progress that someone will fund the next leg. The day the money hits your account, a countdown starts toward a result you have to produce in front of an audience.

Visual 1 — The translation

What founders hear | What a raise actually means | Who's holding the clock |

|---|---|---|

Validation | An obligation to grow into the price someone paid | Your cap table |

Runway | A deadline to show enough for the next round | The next investor |

Fuel for the vision | A mandate to spend faster than feels safe | The board |

A vote of confidence | A bar that just moved up, not down | The market |

Freedom to build | Less freedom — you now answer to owners | Your shareholders |

Read the right-hand column before you sign. Every comforting word on the left has a colder, more accurate translation. The raise doesn't relax the pressure on the business — it formalizes it.

The valuation trap

Here's the mechanism founders feel last and understand worst. The number you're celebrating — the valuation — is not a description of what you've built. It's a target you've agreed to grow into.

Raise at a mark that's two years ahead of your fundamentals and you've just borrowed against a future you haven't earned. It feels like a win because the headline is big and the dilution looks small. But that high mark is now the floor for the next round. You have to grow into it before you can grow past it, and if the business matures slower than the price implied, you arrive at the next raise with a valuation you can't beat. That's the down round, the recap, the cram-down — and they all start with a number that once felt like a trophy.

A high valuation isn't a measure of how far you've come. It's a measure of how far you now have to run before you're allowed to raise again.

The cleanest companies often raise at marks that look conservative and feel slightly disappointing on the day. They've traded a smaller headline for the thing that actually compounds: room to outperform their own price.

Dilution and control as real costs

The other invisible line item is ownership. Every round trades a slice of the company for the money, and the slices stack. Founders who tell themselves "we'll make it up in the next round" usually discover that the next round dilutes them again, and that by the time the company is worth something, they own a fraction of a thing they built and increasingly steer by committee.

Control leaves quietly, in board seats and protective provisions and the soft gravity of a lead investor whose opinion you start anticipating before they voice it. None of this is sinister. It's the deal. But it's a cost, and the celebration culture pretends it's free.

When raising is right — and when it's avoidance

None of this is an argument against raising. There are businesses that genuinely need it: a true land-grab where the market goes to whoever scales first, a capital-intensive build where you can't bootstrap the factory, a winner-take-most category where being second is being dead. In those, the right move is to raise aggressively and run.

But a lot of raises aren't that. A lot of raises are a way to avoid the harder, less glamorous work of getting a business to pay for itself. It's easier to pitch a future than to charge for the present. Fundraising can become a substitute for selling — a way to keep the company alive on belief while postponing the day the unit economics have to make sense. When the deck is more polished than the income statement, the raise isn't ambition. It's procrastination with a wire transfer.

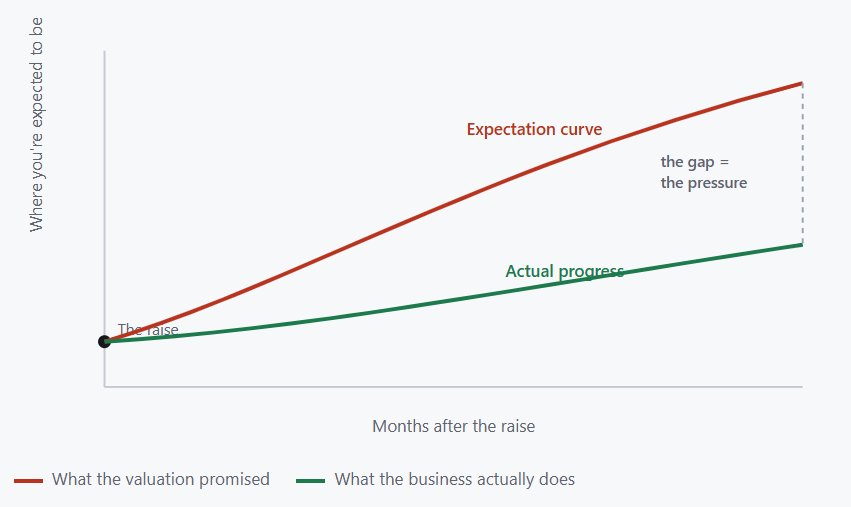

Visual 2 — The gap is the pressure

Conceptual model. The moment you raise, expectations leave on a steeper curve than reality can climb. Every month, the distance between the two lines widens — and that distance is exactly the pressure that ends up on the founder's desk.

The 2026 reality

This used to be a softer argument because capital was nearly free and the next round felt inevitable. Neither is true now. With the cost of capital sitting at a structurally higher plateau and investors back to underwriting on fundamentals rather than momentum, money has gotten both expensive and selective. The bridge round you assumed you could always get is no longer a given. The market that once forgave a missed plan now reprices it.

Which means the obligation a raise creates has more teeth than it did three years ago. You're growing into a higher mark with less margin for error and no guarantee the next check appears. In that environment, raising less — or not raising — stops looking like timidity and starts looking like control.

What this means for founders

Treat the raise as a liability on the balance sheet, not a line in your highlight reel. The day it closes, the only honest question is what you now owe and to whom. Celebrate the renewal, the profitable quarter, the customer who can't live without you. Those are milestones. The raise is the invoice you've agreed to pay them against.

Price for the company you have, not the one you're pitching. A modest valuation you can beat is worth more than an impressive one you have to chase. Optimize for room to outperform, not for the size of the headline. The founders who sleep best raised at marks that looked unremarkable and then made them look cheap.

Earn the right to stay independent. The most ambitious move available to many companies in 2026 isn't a bigger round — it's a path to profit that lets you decide whether to raise at all. Capital you don't need is the only kind you can take on your own terms. Get the business to pay for itself, and the raise becomes a choice instead of a rescue.

The confetti is fine. Enjoy the Thursday. Just don't confuse the moment the money arrived with the moment the work paid off. One is a transaction. The other is the whole point.

A LookatBusiness original. Macro context reflects a higher, more persistent cost of capital and a more selective funding environment in 2026, in which bridge and follow-on rounds are no longer assured and investors increasingly underwrite on fundamentals rather than momentum. Scenarios are composite and illustrative.