The same trait — refusing to quit — makes some founders legends and bankrupts others. The difference is knowing which situation you're actually in, and almost nobody can read it from inside.

Two founders, same week, same story. Each has spent three years on a product the market keeps shrugging at. Each is down to a few months of cash. Each looks at the wreckage and decides to keep going — same jaw set, same speech to the team, same refusal to hear the word quit.

One of them is about to break through. The other is about to lose everyone's money. And here's the uncomfortable part: standing where they're standing, in that week, neither can tell which one they are. From the inside, the founder who's right and the founder who's deluded are running the identical script.

Grit and delusion look the same

We have a whole mythology built on persistence. The founder who was told no a hundred times and kept going. The idea everyone mocked until it was obvious. These stories are real, and they're also a survivorship trap, because the founders who kept going on a genuinely dead idea don't get profiles written about them. They just quietly run out of money, and their persistence gets reclassified — from grit to stubbornness — the moment the bank balance hits zero.

The trait didn't change. The outcome did, and then we renamed the trait to match. Persistence is called vision in the winners and denial in the losers, but only ever in hindsight. In the moment, they are the same thing wearing the same face, and the founder feeling it has no reliable way to know which one is theirs.

Why founders can't self-diagnose

This would be a solvable problem if founders could read their own situation clearly. They can't, and not because they're foolish. The very traits that let someone start a company are the traits that corrupt the read.

The first is commitment bias. Three years and your reputation are sunk into this idea, and the human mind is exquisitely designed to protect a sunk investment by finding reasons it was right. Every ambiguous data point gets read in the direction that justifies continuing. The second is identity fusion. For most founders the company isn't a project — it's who they are. Admitting the idea is dead doesn't feel like updating a business decision. It feels like admitting you are a failure. So the brain does what brains do under that threat: it protects the identity and discards the evidence.

The founder is the single worst-positioned person in the building to judge whether the founder should keep going. Everything that makes them good at starting makes them bad at this one call.

This is the trap underneath the trap. The decision that most needs cold judgment is the one the decider is least equipped to make coldly — and the more committed and visionary the founder, the more compromised the read.

Signal versus noise

So what does a real signal actually feel like, as opposed to a wishful one? This is the whole game, and the difference is subtle but learnable.

Real traction has a texture. Customers come back without being dragged. They tell other people. They get annoyed when the product is down, because they've woven it into how they work. The numbers are small but they move in the same direction repeatedly, and the movement survives you taking your thumb off the scale. A wishful read has a different texture: the wins are loud but don't repeat, the growth needs constant founder heroics to happen at all, and the encouraging signs are mostly compliments rather than behavior. People say they love it. They just don't use it, pay for it, or come back.

The tell is whether the signal persists when you stop pushing. Real demand has its own engine. Wishful demand runs entirely on yours, and the moment you rest, it stops.

Visual 1 — Reading the signal

What you're seeing | Signs to persevere (evidence-based) | Signs to pivot (hope-based) |

|---|---|---|

Retention | Users return on their own and keep returning | You re-acquire the same churned users monthly |

Growth source | It continues when you stop pushing | It stops the week you take a break |

Customer voice | They complain when it breaks — they depend on it | They compliment it, then don't use it |

The trend | Small numbers moving the same way, repeatedly | Big wins that never repeat |

Your evidence | Behavior: usage, renewals, referrals | Sentiment: praise, encouragement, "potential" |

Run your last quarter through both columns honestly. The persevere column is built from things people did. The pivot column is built from things people said. When your case for continuing lives mostly in the right-hand column, you're funding hope, not demand.

The cost of persevering on a dead idea

"Never give up" sounds noble until you price it. Every month spent persevering on something that won't work is a month of cash, a month of your best years, and a month of your team's careers spent on a corpse. The cost isn't just the money you'll lose at the end. It's the pivot you didn't make a year earlier, when you still had the runway and the energy to make it cleanly.

The founders who win are not the ones who never quit. They're the ones who quit the right things fast — who kill a dead idea while there's still time and conviction left to chase a live one. "Never give up" is, for a meaningful share of founders, the single most expensive piece of advice they will ever take. The skill isn't endurance. It's discrimination: persevering only where the evidence supports it, and abandoning everything else without sentiment.

Building outside checks

If the founder can't trust their own read, the answer isn't to try harder to be objective. You can't out-discipline identity fusion. The answer is to build the judgment outside yourself, before you need it, while you're still calm.

That means pre-committed decision lines, set in advance: "If we haven't hit X retention by this date, we pivot — not discuss, pivot." Written down when you're clear-headed, they're a contract with your future, compromised self. It means a small number of people whose job is to tell you the truth, who don't share your sunk costs and won't flinch when you push back. And it means watching behavior, not your own feelings — because your feelings about the company are precisely the instrument that's broken. The point of all this is to take the most important call out of the hands of the person least able to make it: you, in the moment, mid-fusion.

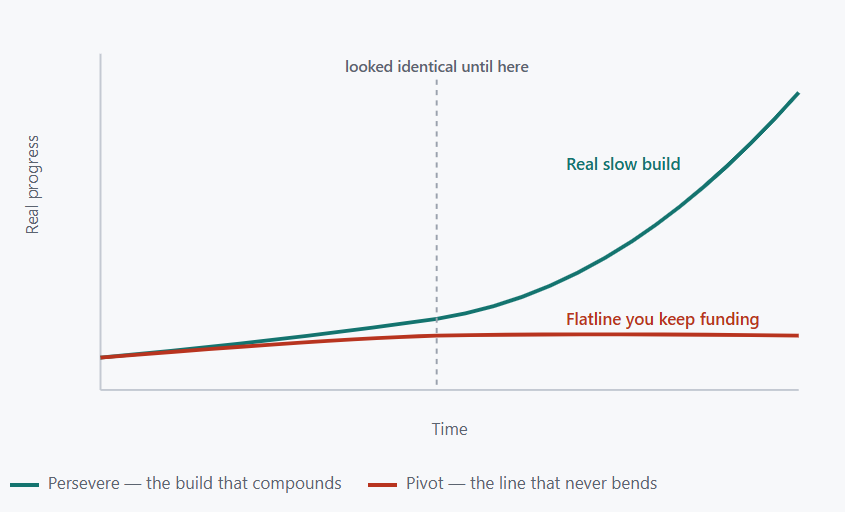

Visual 2 — Same start, different ending

Conceptual model. Early on, the real slow-build and the flatline are indistinguishable — same slope, same patience required. The whole difficulty is that the divergence only becomes visible after the point where you had to commit. Pre-set decision lines exist to force the call before the curves separate, not after.

Pivoting without thrashing

There's a failure mode on the other side, too. Some founders, terrified of being the deluded one, pivot at the first hard week — abandoning ideas before any real signal could have formed, chasing the newest narrative, mistaking motion for learning. That's not discrimination. That's the same wishful pattern-matching, just pointed at the next thing instead of the current one.

A good pivot is evidence-driven and decisive: you saw the signal fail to materialize against a line you set in advance, you killed it cleanly, and you carried forward what you genuinely learned about the customer. A bad pivot is fear-driven and serial: you bailed because it got hard, learned nothing transferable, and reset the clock to zero. The discipline is the same in both directions — persevere only where evidence supports it, pivot only when evidence demands it, and never let either decision be made by hope alone.

What this means for founders

Stop trusting your conviction as a signal. Conviction feels identical whether you're right or deluded — it's generated by your commitment, not by the evidence. The strength of your belief tells you how invested you are, not how correct you are. Treat your own certainty as the least reliable data point in the building.

Write your decision lines down before you need them. Set the metrics and dates that would tell you to pivot while you're still calm and the company isn't on fire. A pre-committed line, made by your clear-headed self, is the only judge your fused, mid-crisis self will be unable to argue away.

Reject "never give up" as a strategy. The founders who win quit dead ideas fast and persevere only where behavior — not praise, not hope — backs them. Endurance isn't the rare skill. The rare skill is knowing precisely what to endure for, and walking away from everything else without flinching.

The two founders from the start of this piece are still standing in that week, still running the same script. The one who makes it won't be the one who wanted it more. It'll be the one who built something outside their own head to tell them the truth — and then was brave enough to listen.

A LookatBusiness original. The founder situations described are composite scenarios drawn from common patterns and do not depict any specific company or individual.