Cutting costs keeps working — that's the danger. Past a certain point you're no longer removing waste, you're removing the company's ability to grow. And the bill arrives in a different quarter than the savings.

Cost cutting has a seductive property: it almost always works the first time, so you do it again. The first round removes obvious waste and margin improves. The board is pleased. The second round is harder but still lands. By the fourth, you're not finding fat anymore — but the discipline has become a reflex, and the P&L still rewards it this quarter, so you keep going.

That's the trap. Efficiency is self-reinforcing in a way that masks the moment it turns destructive, because the savings show up immediately and on this quarter's statement, while the cost shows up later, somewhere else, and never with your name on it. By the time the damage is visible, it reads as a market problem or an execution problem — anything but the thing that actually caused it.

Why this trap is wide open right now

Two forces have made cutting more fashionable, and more dangerous, than it's been in years.

The first is the cost of money. With capital sitting at a structurally higher plateau and boards rewarding capital efficiency over expansion, every dollar of cost now competes against a real hurdle rate. That's a healthy correction after a decade of cheap money funding bloat — but it also creates relentless pressure to keep cutting well past the point of usefulness, because each cut still flatters the return on capital.

The second is AI, which has made cutting feel free. The pitch is everywhere: automate the function, thin the team, hold output flat at lower cost. Sometimes that's real efficiency. Often it's removing the people who held context, absorbed the weird cases, and noticed problems early — capacity that doesn't show up in a headcount line until it's gone and something breaks that used to get quietly caught.

The three things a cut can remove

Every cost cut takes one of three things off the table. They look identical on a spreadsheet and behave nothing alike.

Waste. Cost that produces no value — duplicated tools, a process nobody needs, spend that survives only out of habit. Cutting waste is pure gain. There's no later bill. If all your cuts were here, the trap wouldn't exist.

Resilience. Cost that produces no value until something goes wrong — the slack, the redundancy, the experienced person who isn't fully utilized on a normal day. On a spreadsheet it's indistinguishable from waste, which is exactly why it gets cut. Then a shock arrives, and the thing that would have absorbed it isn't there. The savings were booked in Q1; the failure lands in Q3 and gets blamed on the shock, not the cut.

Growth. Cost that produces value later — the maintenance, the R&D, the brand, the team capacity that next year's expansion runs on. Cutting it is the cleanest-looking decision of all, because nothing breaks immediately. The company just quietly loses the ability to grow, and discovers it a year later when the pipeline that should have been building never built.

Visual 1 — What the cut removed, and when the bill comes

The cut removes | Looks like on the P&L | When the real cost lands | Who gets blamed |

|---|---|---|---|

Waste | Clean savings | Never — it's free | No one (correctly) |

Resilience | Identical clean savings | Next shock or outage | "Bad luck," the market |

Growth | The cleanest savings of all | A year out, in lost expansion | Sales, the strategy, the cycle |

The core problem: all three look the same when you approve them. The trap is that the two expensive kinds are the ones that produce no visible pain at the moment you cut — so they're the easiest to cut and the ones you most regret.

Lean is not the same as strong

The deeper hazard is that efficiency and resilience trade against each other, and most operating cultures only reward one of them. A perfectly efficient system has no slack — every resource fully utilized, no redundancy, no buffer. It also has no capacity to absorb anything unexpected. Maximum efficiency and maximum fragility are the same state viewed from two angles.

A company optimized to the last dollar isn't strong. It's tuned for exactly the conditions it was optimized in — and priced for disaster the moment those conditions change.

This is why the leanest competitor in a sector is often the one that doesn't survive a real shock. It didn't get unlucky. It spent its margin for error in advance and called the spending "discipline."

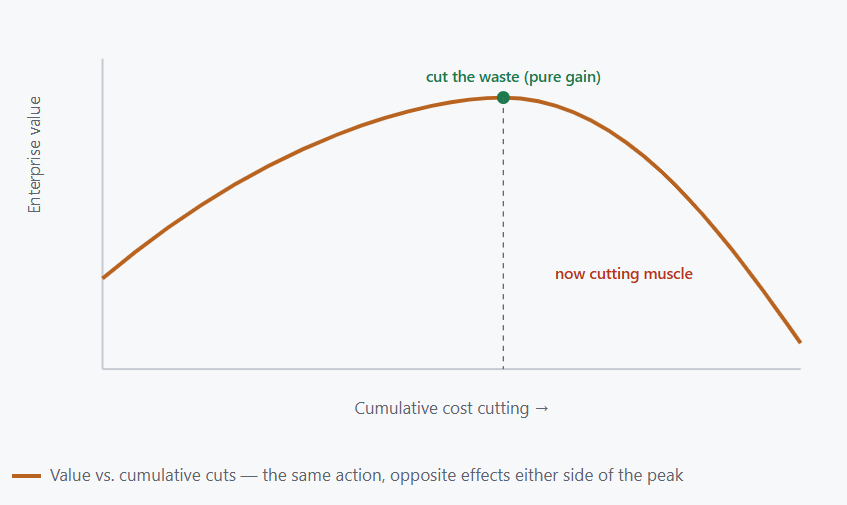

Visual 2 — The efficiency curve

Conceptual model. The first cuts add value by removing waste. Past the peak, the identical activity destroys it by removing resilience and growth. The trap is that nothing tells you you've crossed the peak — the P&L keeps improving for a while either way.

What this means for leaders

Before approving any cut, force the question the spreadsheet can't ask: which of the three is this — waste, resilience, or growth? If you can't tell, treat it as resilience or growth, because those are the ones that look like waste right up until they cost you. The burden of proof should sit on "this is genuinely waste," not on the person trying to protect the capacity.

Hold a deliberate amount of slack and call it what it is — an investment in optionality, not laziness you haven't gotten around to removing. The right level of efficiency is never 100%. A system run at the red line has traded its entire capacity to respond for a few points of margin, and that trade is almost always underpriced.

And watch the lagging indicators, not just the quarterly win. Margin improving while cuts continue is not proof the cuts are working — it's exactly what the trap looks like from inside. The real signals show up later and elsewhere: slower recovery from problems, capacity you used to have and now don't, growth that quietly stops compounding. If those are moving the wrong way while margins look great, you're not running a tight ship. You're spending the ship for parts.

Context drawn from: RSM, "When Money Has a Price", Norton Rose Fulbright, Cost of Capital: 2026 Outlook, and Morgan Stanley Counterpoint Global, "Cost of Capital and Capital Allocation."