For fifteen years, near-free capital wasn't just the backdrop to how companies were built — it was a hidden operating assumption baked into all of it. That assumption has now been repriced, and most playbooks haven't noticed.

An entire generation of operators learned to run a business under one unspoken assumption: capital is nearly free, and you can always raise more. It was never stated as strategy. It didn't have to be. It was the water everyone swam in — the condition that quietly shaped what got funded, what got rewarded, and what counted as a smart move.

That assumption was a business model in disguise. And it has just been repriced — not for a cycle, but, on the evidence, for the foreseeable future.

What cheap money was actually paying for

When money costs almost nothing, the entire logic of building a company tilts in one direction. Growth beats profit, because a dollar of future revenue is discounted so lightly it's nearly as good as a dollar today. Scale beats margin, because you can fund the losses until scale arrives. Experiments are cheap, so you run dozens. Acquisitions are cheap, so you roll up. And a compelling story about the future is worth more than cash in hand, because the future is barely discounted at all.

None of that was irrational. It was a correct response to the price of money. The problem is that a decade and a half of it hardened into instinct — into how a whole cohort of founders, operators, and investors understand what "good" looks like. Burn to grow. Raise on narrative. Optimize for the next round, not the next dollar of profit. Those weren't preferences. They were the cheap-money model, internalized as common sense.

Why this is a regime, not a dip

The easy thing to believe is that this is temporary — rates spiked, they'll come back down, the old playbook will work again. The signal from the people who set the price of money says otherwise.

The Federal Reserve has raised its estimate of the long-run neutral rate to its highest level in a decade — north of 3% — which is its way of saying the floor itself has moved, not just the ceiling. Markets that once priced in a steady series of cuts are now pricing in barely one for the year. "Higher for longer" has stopped being a warning and become the baseline. The plateau, not the peak.

This isn't the tide going out and coming back. It's the sea level changing. The businesses built for the old water line are now operating in a different ocean and calling the difference a rough patch.

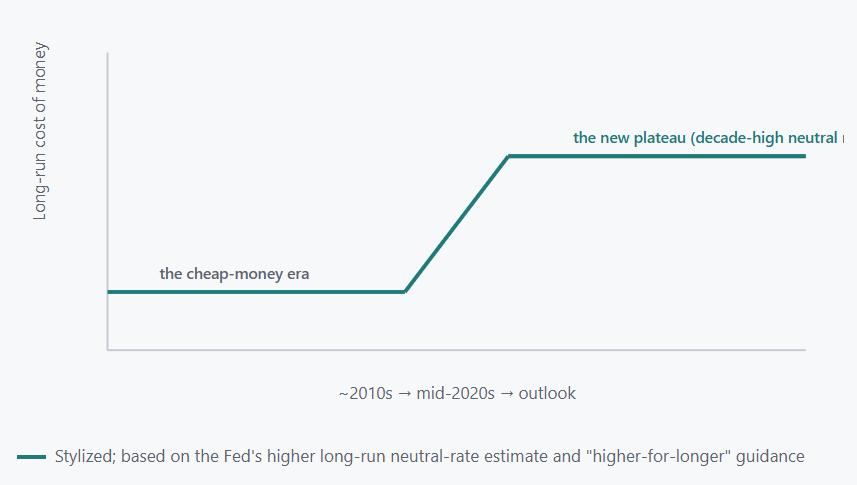

Visual 1 — The floor moved, not the ceiling

Illustrative, not to scale. The point isn't the exact number. It's that the resting level of the cost of capital stepped up to a new plateau — and the business assumptions calibrated to the old one are now mispriced.

What just got repriced

When the cost of money resets, a lot of things that looked like permanent truths turn out to have been features of the old regime.

Visual 2 — Old assumption, new reality

Cheap-money assumption | Higher-cost-of-capital reality |

|---|---|

Growth now, profit later | Profit is the growth; the "later" got expensive to wait for |

Capital is always available | Capital is selective and priced; the next round isn't guaranteed |

Scale will fix the margins | Margins have to work at the scale you're at now |

A great story commands a premium | Cash generation commands the premium; narrative is discounted |

Run many cheap experiments | Every bet competes against a real hurdle rate |

What it shows: none of the left column was wrong in its era. It's that each item was a response to a price that has changed — and the right column is what the same logic produces at the new price.

The contrarian read: this is good news for the right companies

It's tempting to frame all of this as loss — the end of easy funding, harder building, a colder market. For the companies that mistook cheap capital for a strategy, it is. But a regime where money has a price is not worse for everyone. It's a transfer of advantage.

When capital was free, financial cleverness could beat operational quality — you could out-raise a better-run competitor and buy the market. When money has a price, that edge erodes, and the advantage moves back to the boring virtues: real margins, durable cash flow, the discipline to make a dollar do a dollar's work. The operator who was quietly profitable through the cheap years and got called unambitious for it is now holding the rarest asset in the room — a business that doesn't depend on someone else's willingness to keep funding it.

There's a generational wrinkle that makes this harder than a normal cycle. A large share of today's leaders have never operated a company in this regime. Their entire professional model of "how business works" was formed under conditions that no longer hold. That's not a knock on them — it's a warning that the instincts they trust were trained on a different world, and the ones who'll do well are the ones who notice that and retrain rather than wait for the old water to return.

What this means for leaders

Audit your strategy for cheap-money assumptions you've never questioned. Anywhere your plan quietly depends on "we'll raise again," "scale will fix the unit economics," or "growth justifies the burn," you may be running a model calibrated to a price of money that no longer exists. Those assumptions don't announce themselves — they're load-bearing and invisible until they fail.

Treat cash generation as a strategic asset, not a consolation prize. In a world of selective, expensive capital, the ability to fund yourself is leverage — over competitors who can't, over investors who know you don't need them, over a future you can't forecast. The companies that compound from here will be the ones least dependent on the kindness of the next round.

And stop waiting for the rates to come back. The most expensive thing a leadership team can do right now is run the old playbook a little longer in the hope the environment reverts to it. It may not, and the cost of assuming it will is paid in exactly the years you can't get back. Build for the sea level you're actually in — not the one you learned to swim in.

Context drawn from: Fed long-run neutral-rate guidance, March 2026, RSM, "When Money Has a Price", and Norton Rose Fulbright, Cost of Capital: 2026 Outlook.